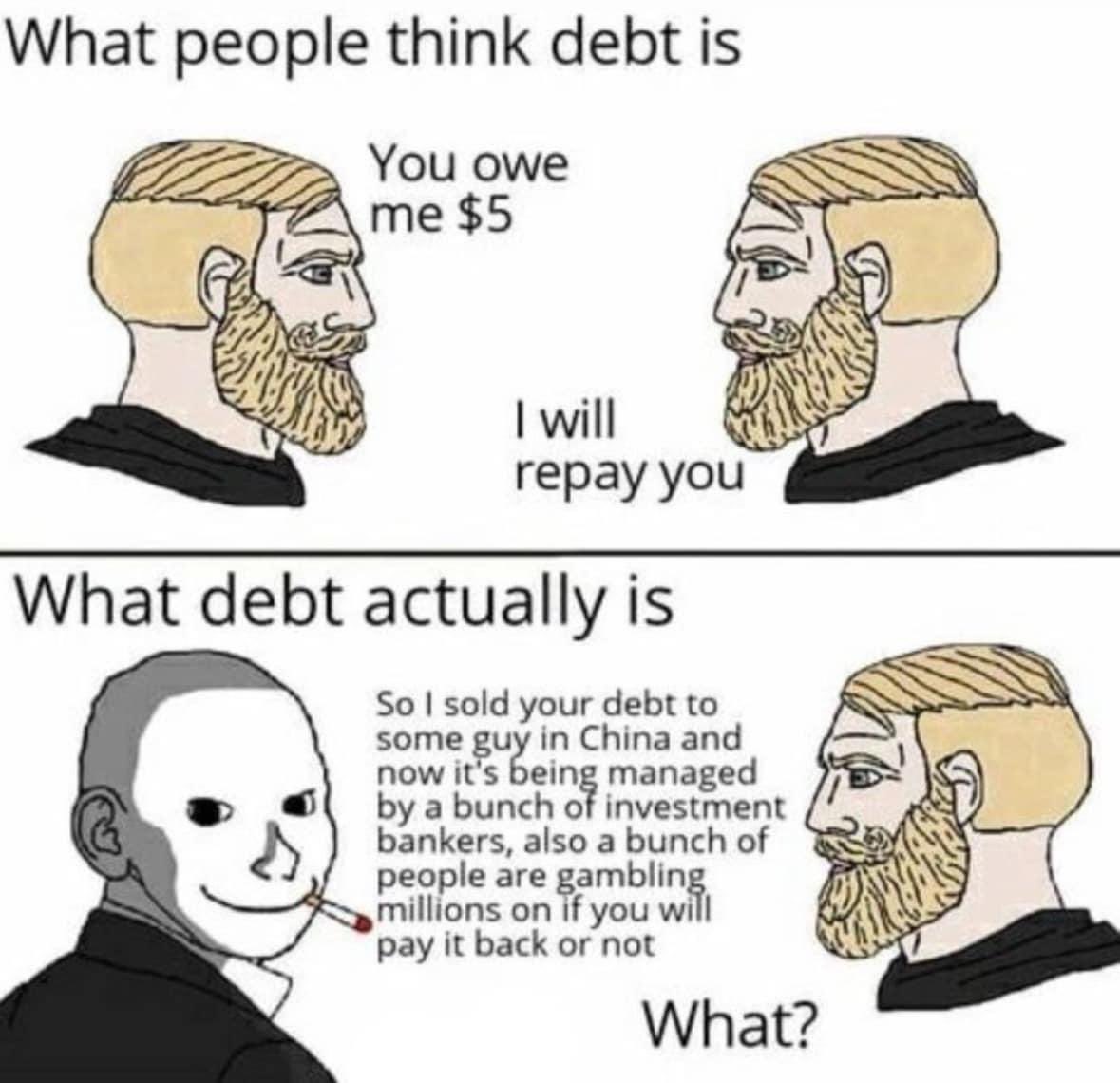

What it actually is:

We’ve given big, privately owned banks the right to create money out of thin air.

They lend it to you for a while, if you can prove that there’s no risk involved.

You still have to pay them back a lot more than you got.

Once you’ve given the money back, it disappears.

The banks keep the interest, though. And can use it to create 10x more money out of thin air.Man, if it were just this then banks would be pretty stable.

The problem is banks don’t just lend and receive money, they invest. And they invest in everything. And they take super risky bets.

This is what caused the banking collapse of 2008 and what caused the death of SVB and a few other banks.

Your bank doesn’t just hold your money and debt, if you rent it almost certainly owns a peice of the company managing your property. It owns crypto assets. It has shares of startups. And it uses those assets to get more money to create more debt.

Dobb Frank was created to stop some of this, but unfortunately it’s been effectively repealed already.

Yup, and banks are returning to high-risk securities, trading in debt-based products like collateralized loan obligations, just like they did leading up to the 2008 global financial crisis.

Bank: You should take out this loan you can’t afford to repay. Don’t worry, we’ll make it seem like a great idea.

Unqualified borrower: Ok, since you made it seem like a great idea.

Bank: Great! Hey, other bank, betcha this guy won’t repay this loan.

And Dodd-Frank was passed as a weak facsimile of the previously-repealed Glass-Stegall act that was written after the Great Depression and effectively prevented any major financial collapses for 70 years.

1000%

It’s not out of thin air, it’s out of your account, and everyone else’s too. They’re banking (heh) on most people not needing most of their money all at once. They keep a required reserve amount for people to actually withdraw. If all of the sudden everyone wants all of their money then that’s a run on the bank and it collapses.

No, it is actually out of thin air.

When a bank gives out a credit, that money is created on the spot, not drawn from somewhere.

There are rules as to how much money a bank is allowed to create, based on how much they actually have.

But no account of any kind is reduced by the amount they give out as credit.When a bank gives out a credit, that money is created on the spot, not drawn from somewhere.

Incorrect. Try starting your own bank and doing that. No other banks will do business with you and you’ll run out of money to give your borrowers.

This is how banks work.

You deposit 100 and I deposit 100, bank is required to keep 10 percent in cash (for example) that allows for 180 in loanable cash.

The bank loans out 180 dollars, now you have 100, I have 100 and someone else has 180, that money has been ‘created’ out of thin air.

The banks count on the fact that that me and you won’t both withdraw all of our money at once.

When banks finish the day, they actually check and see if they are within all of the margin limits that are required and do overnight loans from other banks to stay legal.

Look up fractional reserved banking.

bank is required to keep 10 percent in cash

Not correct. Your liabilities need to be sufficiently smaller than your assets. Capital reserves don’t need to be in cash.

someone else has 180, that money has been ‘created’ out of thin air

200 dollars went in. 180 dollars came out. 20 dollars stay in the bank. No dollars have been created.

Look up fractional reserved banking.

Look up solvency frameworks

Money hasn’t been printed, but for the bookkeeping, 3 individuals who have contributed a total of 200 dollars, have in their accounts 380 dollars.

When a bank loans your money out, as we are well aware, they don’t change the account in your balance. In order to do that, the dollar being loaned must be duplicated somehow. This is normal to how fractional banking works, and guidelines and requirements for how much specific money you need to maintain doesn’t change that.

The only way to change it is to switch to full reserve banking.

If a bank is able to loan out your money, without also removing it from your account, it is by nature created, the money is in two places at once.

Money hasn’t been printed, but for the bookkeeping, 3 individuals who have contributed a total of 200 dollars, have in their accounts 380 dollars.

Person A’s account: $100 Person B’s account: $100 Person C’s account: -$180

This does not add up to $380.

They don’t reduce your available balance because they’re constantly juggling the money around. But they’re not producing money out of thin air. They can’t loan more than they hold in deposits.

Uh… Yeah they can? Look up fractional reserve banking.

no but y y youre youre youre youre y you’re saying the money’s in Joe’s house, th thats that’s right next to yours, and and and and the Kennedy House, and Mrs Maitlin’s house and a hundred others.

w w why w why why why whaddaya want the Moon, Mary? L L L Lemme throw a LASSoo around it.

I sampled that scene in one of my songs.

Precisely. That scene made so much more sense to me after I took a financial accounting class in college.

Yep. Just don’t borrow it, fuck em.

Unless you’re really rich, you have the choice between borrowing money from the bank, and paying rent to a landlord for your entire life.

Unless you’re moderately rich, you don’t even have that choice.If people could buy housing without needing to borrow money, the world would be a much better place.

The derivatives market is out of control. The global annual GDP, actual goods and services produced, is something like $100 trillion. The derivatives market is something like 7 times that.

About 80% of the global economy is just gambling on what the other 20% will do.

A derivative != gambling what the other 20% will do.

A common derivative is a “future”.

Pre-ordering a videogame is a future contract. It’s a way for game publishers to finance the development of the game.

Sometimes futures are the only way to trade a product: all electricity is sold under a future contract. This refers to producers and consumers agreeing “tommorow 11am to 12am, I will consume (for the one party), and produce (for the producing party), 10MW of power”. It is a simple necessity to trade electricity as a future contract, as electricity isn’t easily stored, and the grid needs to be balanced (production ~= consumption) at all times. Here, the future contract is used as a method of coordination.

Futures are still technically gambling. In some cases a very, very safe gamble, but it still boils down to promising a predetermined price for a future transaction. There’s always a chance that the underlying asset radically changes in value between the contract and execution dates.

I don’t deny that derivatives are certainly financial instruments with valuable use cases. I’m just saying the scope of that market is out of control, especially in regards to financial derivatives. The MBS market basically directly lead to the '08 crisis, as you certainly know.

Futures are still technically gambling.

If you enter into a futures contract to fix your costs (electricity, oil, steel etc.) then you are reducing your risk. This is the opposite of gambling.

Sometimes doing nothing is the risky option.

Every transaction has a counter-party. Reduced risk on one side increases risk on the other.

Not necessarily. Two companies in different countries can both reduce their risk by entering into an FX swap.

I didn’t know enough about FX swaps to comment personally, but Investopedia says this:

The top risk with foreign currency swaps is currency risk. Currency risk arises from fluctuations in exchange rates between two currencies involved in the swap. When companies or financial institutions enter into a swap, they agree to exchange cash flows in different currencies at future dates. If/when the exchange rate moves, one party may end up paying significantly more in its domestic currency than anticipated. For example, if a company swaps U.S. dollars for euros and the euro strengthens, the company will need to pay more in dollars to meet its euro obligations.

Another key risk is interest rate risk. Foreign currency swaps often involve exchanging fixed or floating interest payments on the notional amounts of the two currencies. If interest rates in one country rise unexpectedly, the party receiving fixed interest payments in that currency may miss out on higher interest income. If interest rates decline, the party paying floating rates could face higher-than-expected costs.

Counterparty risk is another risk. In any swap agreement, the parties involved rely on each other to fulfill their obligations. If one party defaults, the other party may face financial losses. To mitigate this risk, companies often perform thorough due diligence on their counterparties or utilize clearinghouses for swap agreements. As is the case with most financial instruments, this risk cannot be eliminated.

Last, the liquidity risk associated with foreign currency swaps is another factor to consider. These swaps typically have long maturities, and the liquidity of certain currencies can fluctuate over time. If market conditions change and a party wants to exit the swap early, they may find it difficult to find a willing counterparty, especially if they wish to trade or exchange out of their position.

Company A sells widgets for dollars made from raw materials bought in yen.

Company B sells woggles for yen made from raw materials bought in dollars.

Both companies can reduce their risk by agreeing to exchange yen for dollars at an agreed fixed value. No one is gambling. Everyone is reducing their risk.

Interest rates, some companies may have floating income they wish to swap for long term fixed, and others may have too much long term debt which has a volatile mtm value.

Counterparty risk, usually mitigated by diversification. Companies pool their specific risk for a lower, but more certain, general risk (and use clearing houses).

Liquidity risk. Only a problem if you need to sell something quickly. Here there are gamblers taking advantage. There’s no-one that naturally wants to take the other side of illiquid assets.

In isolation. But let’s look at insurance, to the consumer it’s the opposite of gambling. Gambling is seeking excitement through financial risk, but insurance is accepting that all of life is risky and that you’d rather pay a flat rate every month not to bother with the risk. But to the insurance company it’s not like they’re just holding and waiting, no they’re firstly pooling enough people to attempt to make payouts as stable as possible. Your house burning down is one of the worst days of your life, but it’s just another day at work to the fire department and insurance company, they see that sort of thing regularly. Additionally they hire actuaries and statisticians to minimize their risks and to make sure they aren’t charging people little enough they go under if they have a bad week or month. It’s why you can’t buy house insurance in Florida anymore, they’ve accepted that climate change has resulted in too much volatility in that area and that they wouldn’t be able to get people to pay the cost necessary to sufficiently hold that risk.

Firstly, insurance isn’t a derivative, so it’s not really relevant here.

Secondly, paying insurance is still a form of financial risk. If you pay insurance for the entire time you own a home, but never file a claim, then that’s basically just money wasted. You’re trading material risk to your home for financial risk.

And it’s also basically a gamble. You’re betting that the total you pay in premiums will be less than whatever the insurance company will pay you. The insurance company is betting that it’ll be higher.

deleted by creator

Futures are still technically gambling. (…) There’s always a chance that the underlying asset radically changes in value between the contract and execution dates.

Sure, I agree. But in the same technicallity; purchasing or selling anything is technically gambling, there’s a chance that it will devalue or increase in value over time. You could’ve bought (or sold) earlier (or later). (Electricity market, again, being an interesting exception, as the product is destroyed as soon as it’s created. One could say the true value is never discovered, as it’s only sold as futures).

The MBS market basically directly lead to the '08 crisis, as you certainly know.

The fundamental problem that lead to the '08 crisis was incorrectly priced mortgages, and risk of repayment/devaluation. Even if the morgages were held by the original issuers, the same outcome would’ve occured.

It wasn’t the derivative market that was the problem.

An example of a derivative, that I can’t think of any reason for existing, other than increasing risk, are leveraged ETPs. I’d call those as close to pure gambling of any derivatives I know of.

Those mortgages were priced incorrectly because the derivatives market inflated their value. There were other factors that contributed certainly. The credit rating agencies certainly played a critical role, but they were incentivized to inflate their rating because of the MBS market.

The regulation of these markets was also to blame, and that’s a whole other can of beans, but again this was due mostly to the revolving door between the regulatory agencies and the investment funds that profit from lax regulation of the derivatives market.

shouldn’t gambling be defined as a strictly asset lacking market environment? Meaning there is no actual value within the trading being done, and the fact that it is purely and entirely speculative on nothing other than “optimal odds”

Where as the market in question would be defined more accurately as a potentially unstable (as all markets are, welcome to capitalism) commodity trading marketplace.

Gambles on failure of stocks shouldn’t be allowed, regulate wall street WS. They will make off like bandits when the tariffs hit.

They will make off like bandits when the tariffs hit.

well then you would be a very bad investor to not jump in on the market hype, assuming your statement is right and that everything will implode.

I disagree. That’s like saying insurance shouldn’t be allowed.

Highly regulated would be anotheratter though.

Nah wall street as it is should absolutely not be allowed, frankly speaking I think stocks should be locked down to regions not just countries. Also regulations are good. I will note that I am generally against the concept of large regional corporations let alone multinational ones, so that side of things is certainly effecting my opinion. Also logistics and trade companies are the exception even if I wiould replace them all with Teamster syndicates.

The derivatives market is something like 7 times that.

The notional value is that size, but that’s not really representative. You can’t compare or even add notional amounts.

For example, temperature derivatives would have a notional value measured in millions of °C.

Well put

Holy crap some source on these numbers? Not doubting them just want to read more about it.

It was what popped up with a quick search. It’s a difficult thing to accurately calculate, but estimates of the total derivatives market can be up to $1 quadrillion. Again, there are difficulties measuring and calculating this, but it’s absolutely massive by any measure.

While funny, and this is a the meme community, God it’s so much worse than that. Debt accumulated in a western style capitalist society is just how money exchanges hands. Your debt, the one that deeply affects your life, that can ruin your ability to make basic purchases and health care is a simple gamble for the rich, OUR debts.

Their debts are waved away, all because it makes more profits to forgive major mistakes when the other people are rich. I’m looking at you GM and Chrysler, I’ll never forget.

Edit: I forgot.

Wasn’t Ford the American auto company who didn’t have to be bailed out by taxpayers while GM and Chysler did?

Maybe. Listen, what I said was in the moment. You can’t blame me for being stupid on the internet lol.

You just need to be more careful.

I’ve never been wrong about anything online. How could that even happen?

Asymptotically Correct (Wrong in this instance)

Your debt, the one that deeply affects your life, that can ruin your ability to make basic purchases and health care is a simple gamble for the rich, OUR debts.

well no, so there are technically two types of debt, personal debt, the kind of shit you have on your car or house. Which are generally negative, and then investment based debt, a debt that is presumed on the potential future evaluation of a company for example. This is inline with how a lot of VC funding is done, although more complex.

There’s also the concept of having asset backed debt, for example a car, or a house. The downside here is that cars and houses are generally very important to daily life, but if your debt is based on the valuation of your company for example, that inherently holds significantly less personal risk to you.

There’s also a much more complex macro economic theory, where if extremely large players go down, a significant portion of the economy also goes down. It might be beneficial for a government to absolve the debt of a national company if for example, it protects broadly from a significant economic retraction, similar to the kinds we’ve seen before like in the great depression. Granted in that case, we did nothing, and everything imploded, globally.

Money is literally an “I owe you”

When money was first used, instead of exchanging an apple for an orange, X amount of apples is exchanged for a dollar. The dollar is the buyer saying “I owe you” to the seller.

When the apple seller now use the dollar on something else, that’s just selling the “I owe you” in exchange for something else.

Spending money is just selling debt.

(At least that’s how money has always worked in my mind. Listen, economy is weird, idk how this shit works, I’m just coming up with my own explanation okay.)

Historically, debt existed before money existed. But that only works in a framework where people can trust eachother to repay the debt.

Debt: The First 5000 Years by David Graeber is a cool book about this whole topic

I also liked Economics of Money and Banking, a course by Prof. Mehrilng of columbio university, which is available through coursera (1).

It’s not the buyer saying “I owe you”, but the issuer of the currency (actually, usually just the notes, coins are considered to have value). The first person/entity to get the note gave, or promised, the issuer (usually the central bank) something of value, and the issuer gave them a token (note) saying the bank owes the holder of that note a certain amount of value. The recipient can then trade that note freely, as can future recipients, in the knowledge a vendor will accept it for its face value. So, yes, you’re trading debt when you use money, but it’s the bank’s debt to the holder, not the debt of the buyer.

Typically the bank issue money when someone takes a loan, i.e. promises that they will pay the bank the value of the loan plus interest.

I have a bunch of letters from my family dating back to the civil war. It’s fascinating how many IOUs there are in there for like a bushel of apples, or a scrap of leather, or whatever they traded to their neighbors. Like you said, scraps of paper with IOU were literally used like currency, but the real currency was people’s reputation to make good on their debts, the paper was just to track it.

Bartering also assumes, for your example, that the apple farmer wants oranges and the orange farmer wants apples. Consider that either one may not. And then consider how many other goods exist even in primitive agrarian society that people may or may not want at any given time.

Currency is whatever the agreed vehicle is for value exchange that solves this. The apple farmer can now sell apples for silver nuggets and use the silver to buy tools from someone else later, which the orange farmer either doesn’t have or is unwilling to part with. It allows for more complex transactions that then helped grow more complex societies.

No, you’re right! This is exactly why adjusting interest rates by the bank issuing a currency affects how much money is in circulation.

I get why you see it as that but the big thing is that when you have money you basically did something to earn it. You get it after the fact. Well except for the issuer. Debt changes that where you get it ahead of time. Curiously this has been used by the issuer in modern times to determine how much to issue.

doesn’t pay it back

2008 financial crisis

when your puny change in mortgage loan causes upwards of a billion dollars worth of

investmentsgambling to fall apartgambling

it’s not gambling, it’s the equivalent of you putting 60% of all of your life savings into a single stock, which then blips and implodes, making you go completely broke.

It was an incredibly risky investment strategy at the time, because the market was seen as risk negative, essentially.

If it were gambling there would be a 51-49 split in returns somewhere along the way, with hundreds of hours and putting money into machines slowly eating away the money you earn, until you’re left a shriveled husk of a person with nothing to your name.

The 2008 crisis was an example of mass fraud, and I’d be happy to be proven wrong. You can’t point to historical data saying your investment strategy is safe, even tho you completely changed the model. Saying “mortgages are safe” doesn’t mean shit, if to compensate for demand you start handing out mortgages like candy.

I think calling it gambling is quite charitable. And ofc all the

scam artistsbanks got bailed out.The stock market in general is joke. There are so many stocks where it’s an open secret they are fake. Like the Ruble, Tesla and most crypto currencies. The stock market is a world of make believe, where any random decision can change everything. It still fascinates me that the second trump won with his tarifs on EVERYTHING, the stock market grew. What’s next? “Company CEO starts randomly shooting all his employees, stocks reach all time high!”

The 2008 crisis was an example of mass fraud

I guess it mostly depends on how you define fraud.

If i buy something from china, and on the way to the US it falls off the boat and into the sea, destroying it forever, is that fraud?

You can’t point to historical data saying your investment strategy is safe, even tho you completely changed the model.

historical data has nothing to do with the safety of investment. That’s like looking at the fatalities in a war, and deriving the danger from being inside of trenches.

The safety is defined as a component of risk, and stated responsibilities. An extremely safe asset would be something like land, it never moves, doesn’t go anywhere, people will always want it for something. Though it’s not an investment.

A safe investment would be something like a long term diversified stock portfolio, or government bonds.

Risk management is at the core of both investment and gambling. The riskier your investment, the closer it comes to just putting the money on a roulette position in practice. There are plenty of portfolios that slowly hemorrhage money and/or eat up any would-be growth via fees: those are your 51-49 splits. Also it doesn’t matter if there’s such a split if you decide to go all in and it goes belly up, however you slice that.

If you do risky shit with money, it’s a gamble whether it pays off. Maybe I’m misunderstanding the point you’re trying to make?

i would fundamentally disagree, with gambling statistically on average, you always lose. It’s not mathematically possible to win.

This is the reason that things like investment work at all.

It’s complicated, but there are a lot of traders that aren’t very good, and there are a lot of traders that are very good, if you just let the market do it’s natural thing, it has a general tendency to go up. Especially long term, you cannot functionally do this with gambling, you ALWAYS lose.

I would argue that there are risky investments, and then safer investments, and there are really risky investments. None of these are gambling, gambling would be like i said investing most of your life savings, into a particular thing expecting a particular result, with the extreme risk of “losing everything” generally investments are never going to “lose everything” that’s also why you have a broader portfolio.

I think gambling is just a fundamentally different philosophical concept.

I guess theoretically nothing stops you from literally gambling with stocks, but that would be incredibly stupid.

I think you have a very specific definition of gambling which I don’t share. To me, gambling is much broader. Wikipedia summarizes it well:

“Gambling thus requires three elements to be present: consideration (an amount wagered), risk (chance), and a prize.”

That’s it. It doesn’t make an opinion whether the bet is fair. There doesn’t have to be a casino involved at all. It also doesn’t require you to put “most or your life savings” into it for it to be gambling.

I think you are conflating high risk, high stakes and even the precence of a casino into the same concept and call it gambling.

“Gambling thus requires three elements to be present: consideration (an amount wagered), risk (chance), and a prize.”

That definition encompasses everything we do in life. From crossing the road, to buying a fridge, to falling in love.

Exactly! Which is why it is mad trying to outlaw or frown upon “gambling” with stocks.

There are many great wxamples in this thread already of why derivatives are necessary to a functioning society.

You are gambling whenever you get in your car and drive. You are gambling if you get out of bed. You are gambling if you spend too much time in bed.

Risk being present isn’t enough. I think the definition of gambling should include a willful decision to increase the level of risk.

The problem, like with many things in life, is that there’s a desire for people to place clear delineations on things for purpose of clarity and peace of mind, when it actually exists on a very fuzzy spectrum. I’d argue you do gamble a tiny percent chance of getting in a wreck every time you drive in exchange for getting places much faster. Likewise, were you to walk instead, there are unique risks and payoffs associated with that choice too.

Whether or not the risks are well known or there’s a decision to increase the level of risk is a little beside the point. There are plenty of people addicted to gambling who genuinely believe they’ll hit it big and retire one day, and that the reward payout is inevitable even when it’s clearly not.

Some derivatives aim to lower the risk, so the active decision to buy it would be to ungamble then? Or is it just gambling wyen you choose not to buy it?

Do you have insurance on your house or do you gamble that it will be fine without it?

If it were gambling there would be a 51-49 split in returns somewhere along the way, with hundreds of hours and putting money into machines slowly eating away the money you earn, until you’re left a shriveled husk of a person with nothing to your name.

If you get into “The Big Short”, what you’ll discover is that this was effectively what the insurance on the mortgages accomplished. Buying insurance is a losing gambit (also called a hedge) wherein the underlying asset (the policy) loses money over time with the anticipation of a potential windfall at some unspecified event in the future.

What Mark Baum and Michael Burry had done was to effectively buy these insurance plans from the banks themselves, diverting the windfall from a crash into their own pockets. The banks shouldn’t have been auctioning off their insurance (for the same reason you shouldn’t try to sell your fire insurance claims on your house to your neighbor in an effort to turn a profit). But the investment was considered crazy precisely because these insurance plans only ever existed as a fig leaf for regulators and investors (even if we fail, we can’t fail, because we have insurance!) Nobody asked who was going to pay out this insurance or who was going to collect.

My Student loans were sold before I even finished school.

Don’t even ask the question.

The answer is yes, it’s priced in.

Think Amazon will beat the next earnings? That’s already been priced in.

You work at the drive thru for Mickey D’s and found out that the burgers are made of human meat? Priced in. You think insiders don’t already know that?

The market is an all powerful, all encompassing being that knows the very inner workings of your subconscious before you were even born.

Your very existence was priced in decades ago when the market was valuing Standard Oil’s expected future earnings based on population growth that would lead to your birth, what age you would get a car, how many times you would drive your car every week, how many times you take the bus/train, etc.

Anything you can think of has already been priced in, even the things you aren’t thinking of.

You have no original thoughts. Your consciousness is just an illusion, a product of the omniscent market. Free will is a myth.

The market sees all, knows all and will be there from the beginning of time until the end of the universe (the market has already priced in the heat death of the universe).

So please, before you make a post on Reddit asking whether AAPL has priced in earpods 11 sales or whatever, know that it has already been priced in and don’t ask such a dumb fucking question again

Interest

epic troll moment time!

{kind=link}