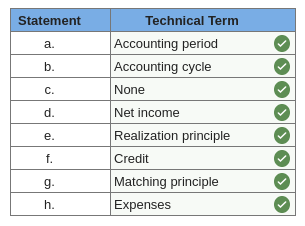

Listed as follows are eight technical accounting terms introduced in this chapter.

Each of the following statements may (or may not) describe one of these technical terms. For each statement, indicate the term described, or answer “None” if the statement does not correctly describe any of the terms.

The span of time covered by an income statement.

The sequence of accounting procedures used to record, classify, and summarize accounting information.

The traditional accounting practice of resolving uncertainty by choosing the solution that leads to the lowest amount of income being recognized.

An increase in owners’ equity resulting from profitable operations.

The underlying accounting principle that determines when revenue should be recorded in the accounting records.

The type of entry used to decrease an asset or increase a liability or owners’ equity account.

The underlying accounting principle of offsetting revenue earned during an accounting period with the expenses incurred in generating that revenue.

The costs of the goods and services used up in the process of generating revenue.

You must log in or register to comment.