- cross-posted to:

- personalfinance

- nyt_gift_articles@sopuli.xyz

- cross-posted to:

- personalfinance

- nyt_gift_articles@sopuli.xyz

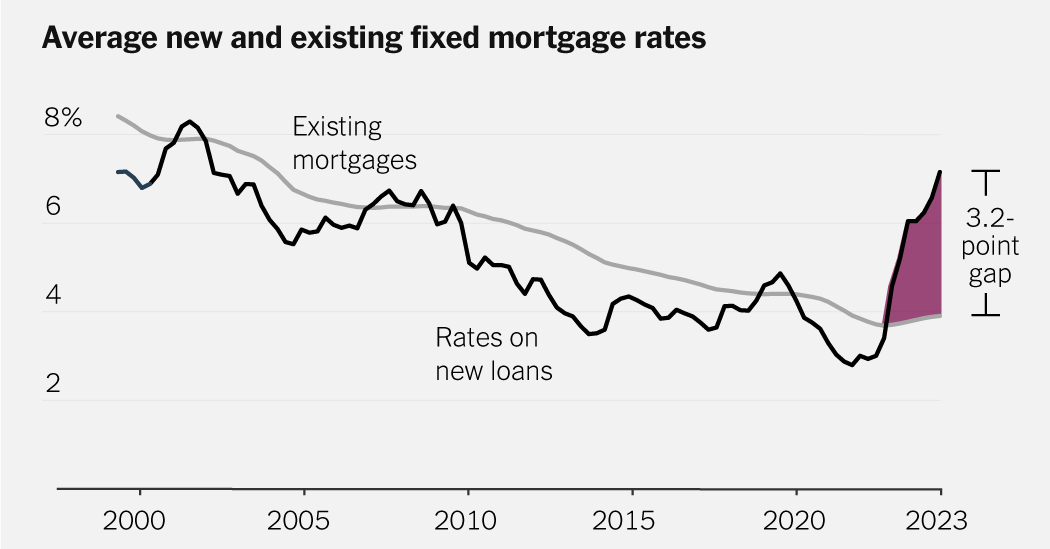

On a scale not seen in decades, many Americans are stuck in homes they would rather leave.

Something deeply unusual has happened in the American housing market over the last two years, as mortgage rates have risen to around 7 percent.

Rates that high are not, by themselves, historically remarkable. The trouble is that the average American household with a mortgage is sitting on a fixed rate that’s a whopping three points lower.

The gap that has jumped open between these two lines has created a nationwide lock-in effect — paralyzing people in homes they may wish to leave — on a scale not seen in decades. For homeowners not looking to move anytime soon, the low rates they secured during the pandemic will benefit them for years to come. But for many others, those rates have become a complication, disrupting both household decisions and the housing market as a whole.

Indeed, according to new research from economists at the Federal Housing Finance Agency, this lock-in effect is responsible for about 1.3 million fewer home sales in America during the run-up in rates from the spring of 2022 through the end of 2023. That’s a startling number in a nation where around five million homes sell annually in more normal times — most of those to people who already own.

Agree, they sound like it’s a problem for people but it’s more of a problem for market. People that are “stuck” with the home they don’t like probably were already struggling to afford even that. It’s not like they were going to just sell it and hop on to another mortgage.

Well, maybe there are such people, and I do agree that mobility is an important thing, but it looks like that level of mobility in choosing a place to live was lost long ago